Презентация "Audit Reports" – проект, доклад

Слайд 1

Слайд 1 Слайд 2

Слайд 2 Слайд 3

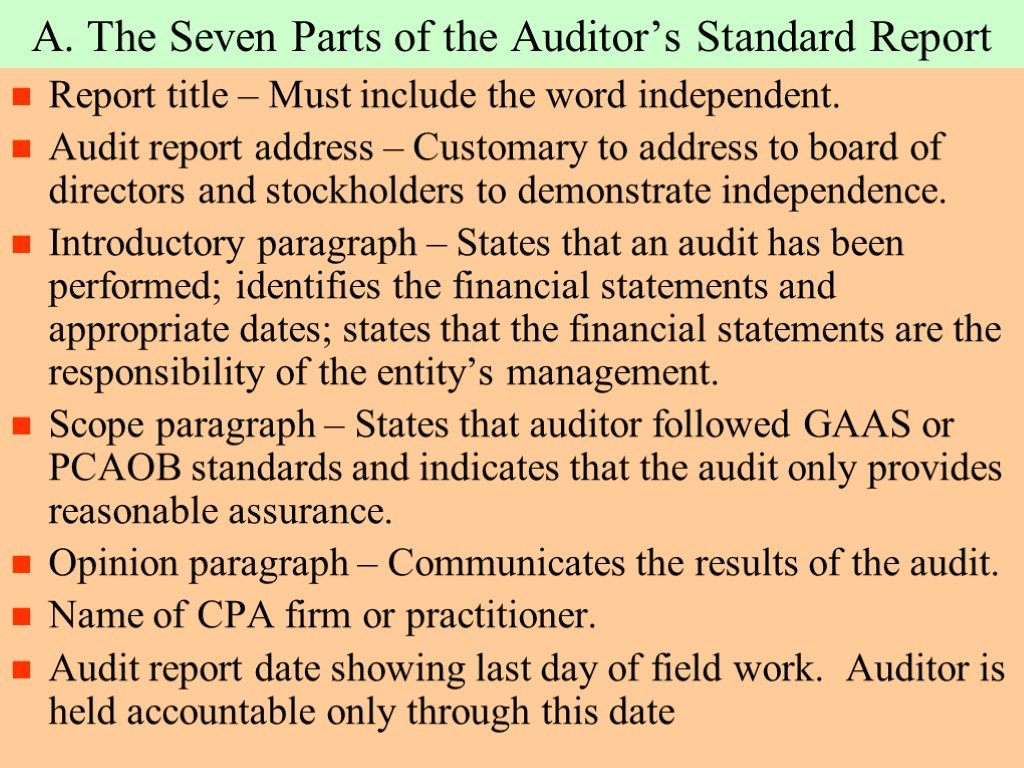

Слайд 3 Слайд 4

Слайд 4 Слайд 5

Слайд 5 Слайд 6

Слайд 6 Слайд 7

Слайд 7 Слайд 8

Слайд 8 Слайд 9

Слайд 9 Слайд 10

Слайд 10 Слайд 11

Слайд 11 Слайд 12

Слайд 12 Слайд 13

Слайд 13 Слайд 14

Слайд 14 Слайд 15

Слайд 15 Слайд 16

Слайд 16 Слайд 17

Слайд 17 Слайд 18

Слайд 18 Слайд 19

Слайд 19 Слайд 20

Слайд 20 Слайд 21

Слайд 21 Слайд 22

Слайд 22 Слайд 23

Слайд 23 Слайд 24

Слайд 24 Слайд 25

Слайд 25 Слайд 26

Слайд 26 Слайд 27

Слайд 27 Слайд 28

Слайд 28 Слайд 29

Слайд 29 Слайд 30

Слайд 30Презентацию на тему "Audit Reports" можно скачать абсолютно бесплатно на нашем сайте. Предмет проекта: Иностранный язык. Красочные слайды и иллюстрации помогут вам заинтересовать своих одноклассников или аудиторию. Для просмотра содержимого воспользуйтесь плеером, или если вы хотите скачать доклад - нажмите на соответствующий текст под плеером. Презентация содержит 30 слайд(ов).

Слайды презентации

Список похожих презентаций

Английский язык Экологические проблемы

Аннотация Проект выполнен на английском языке, что способствует развитию и совершенствованию коммуникативных навыков учащихся. Работа над проектом ...

Мой английский язык

One, two, three, four, Mary at the cottage door, Five, six, seven, eight Eating cherries off a plate. Выучите считалочку. 1 2 3 4 5 6 7 8. Один, два, ...

Английский язык для туристов

Начнем в алфавитном порядке: Австралия. Англия. Голландия. Дания. Ирландия. Канада. Мальта. Новая Зеландия. Норвегия. США. И далее до…. Ямайки! Английский ...

Мой английский язык

Бегут спортсмены разных стран Бежать – запомни, будет run (ран). Шумит, ликует стадион При свете ярких ламп. Отлично прыгнул чемпион! А прыгать будет ...

Английский язык в фокусе

Подготовительный период (3 недели) Распределяли команды, тянули жребий, определяли порядок выступления, номер модуля. Приветствие детей, жюри, гостей ...

Английский язык для тинейджеров. Совершенствуй английский!

Весь мир говорит по-английски! Английский язык - один из самых распространенных языков мира: 1,5 миллиарда людей жителей Земли говорят по-английски ...

Английский язык в 1 классе

Актуальность темы:. Знание английского языка очень важно в современном обществе. Очень важно и продуктивно начинать обучение иностранному языку в ...

Английский язык в деловой и межкультурной сферах общения

Цель: обучение основам делового общения в устной и письменной форме в типичных ситуациях (знакомство, разговор по телефону, корпоративная культура ...

Английский язык

Определение Условные предложения НУЛЕВОГО типа Условные предложения ПЕРВОГО типа Условные предложения ВТОРОГО типа Условные предложения ТРЕТЬЕГО типа ...

Английский язык «Enjoy English»

Полностью завершен курс для 2-11 классов, который включает все компоненты и модули для обучения английскому языку на базовом уровне общеобразовательной ...

Английский язык

В последние годы в связи с расширением международных контактов в наше окружение проникает все больше элементов иностранной речи, особенно английской: ...

Английский язык

REFLECTION: What have you remembered on the lesson today? What was new for you? What lexical material have you memorized today? What information was ...

Английский язык

Прогуляемся по Англии! 1 . Знаменитый магазин игрушек - Hamleys 2. Самая длинная река - Темза 3. Популярный парк - Hyde park 4. Самый старый мост ...

Английский - самый популярный язык

Вряд ли кто знает ! И вряд ли кто-то знает, и даже может себе представить, что когда то английский язык был языком для черни, даже в самой Великобритании. ...

Мой английский язык

LESSON 1 ПРИВЕТСТВИЕ. Hello! –Hi (Хэлоу! –Хай!) Здравствуй! – Привет! How are you? (Хау а ю?) Как дела? I am fine. Thank you. (Ай эм файн, сенк ю) ...

The Role of the Internal Audit Department

Definition of Internal Auditing. “Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve ...

Зачем нужен английский язык

В настоящее время английский язык изучают многие, прекрасно понимая, что знание этого языка необходимо. Очевидно, что зачем нам нужен английский язык ...

Гранжеры.Английский язык

One of the oldest subcultures is granžery, they emerged under the influence of the musical direction of grunge in the 1990-1991year. Its ancestor, ...

Иностранный язык как настольная игра из бумаги

Наиболее популярный способ пополнения словарного запаса при изучении иностранных языков – заучивание слов или фраз с помощью карточек – flashcards ...

Иностранный язык

“He who doesn’t know any language, doesn’t know his own one” Goeth. Научно-практическая конференция 23 мая 2008. Быть или не быть лингвистической ...Советы как сделать хороший доклад презентации или проекта

- Постарайтесь вовлечь аудиторию в рассказ, настройте взаимодействие с аудиторией с помощью наводящих вопросов, игровой части, не бойтесь пошутить и искренне улыбнуться (где это уместно).

- Старайтесь объяснять слайд своими словами, добавлять дополнительные интересные факты, не нужно просто читать информацию со слайдов, ее аудитория может прочитать и сама.

- Не нужно перегружать слайды Вашего проекта текстовыми блоками, больше иллюстраций и минимум текста позволят лучше донести информацию и привлечь внимание. На слайде должна быть только ключевая информация, остальное лучше рассказать слушателям устно.

- Текст должен быть хорошо читаемым, иначе аудитория не сможет увидеть подаваемую информацию, будет сильно отвлекаться от рассказа, пытаясь хоть что-то разобрать, или вовсе утратит весь интерес. Для этого нужно правильно подобрать шрифт, учитывая, где и как будет происходить трансляция презентации, а также правильно подобрать сочетание фона и текста.

- Важно провести репетицию Вашего доклада, продумать, как Вы поздороваетесь с аудиторией, что скажете первым, как закончите презентацию. Все приходит с опытом.

- Правильно подберите наряд, т.к. одежда докладчика также играет большую роль в восприятии его выступления.

- Старайтесь говорить уверенно, плавно и связно.

- Старайтесь получить удовольствие от выступления, тогда Вы сможете быть более непринужденным и будете меньше волноваться.

Информация о презентации

Дата добавления:31 декабря 2018

Категория:Иностранный язык

Содержит:30 слайд(ов)

Поделись с друзьями:

Скачать презентацию

")